Quick Summary

When you export goods or services from India, GST is not simply waived. Your supply is classified as zero-rated, a specific legal status under the IGST Act. Zero-rated means the output tax is 0%, but unlike exempt supplies, you can still claim input tax credit (ITC) on everything you purchased to make that export. This guide explains what zero-rated supply means in practice, the two routes available to exporters, how to decide between them, and the mistakes that delay refunds.

What You'll Learn

- What zero-rated supply means under GST and how it differs from exempt and nil-rated supplies

- How to export without paying IGST using the LUT route, and when to use the IGST refund route instead

- How to avoid the common compliance mistakes that delay or block ITC refunds for exporters

What is Zero-Rated Supply Under GST?

Section 16(1) of the IGST Act defines zero-rated supply as the supply of goods or services either as exports or to a Special Economic Zone (SEZ) developer or unit for authorised operations.

The phrase zero-rated matters. It is not the same as exempt.

Zero-rated supply attracts 0% output tax and still allows you to claim input tax credit. Exempt supply also attracts 0% tax, but you cannot claim ITC on it.This distinction is the reason exporters are protected from the cascading cost of input taxes. Your supplier charges you GST on raw materials, packaging, or services. When you export, you pay no GST on the sale, but you can recover what you paid on inputs, either as a refund or by setting it off.

Zero-Rated vs Exempt vs Nil-Rated: A Quick Reference

| Feature | Zero-Rated | Exempt | Nil-Rated |

|---|---|---|---|

| Output GST | 0% | 0% | 0% |

| ITC on inputs | Claimable | Not claimable | Not claimable |

| GST registration needed | Yes | Sometimes | Sometimes |

| Examples | Exports, SEZ supplies | Healthcare, education | Certain food items |

What Qualifies as Zero-Rated?

Export of Goods

Any goods physically exported out of India qualify as zero-rated. The tax base is the invoice value in the export documentation.

Export of Services

Export of services has a stricter test. Under Section 2(6) of the IGST Act, all five conditions must be met:

- The supplier is located in India

- The recipient is located outside India

- The place of supply is outside India

- Payment is received in convertible foreign exchange (or Indian rupees where RBI permits)

- The supplier and recipient are not simply different establishments of the same legal entity

Miss any one of these, and your service export may not qualify as zero-rated. It may be treated as a domestic taxable supply instead.

SEZ Supplies

Supplies to SEZ units and SEZ developers for authorised operations are also zero-rated, even though the goods or services never leave India physically.

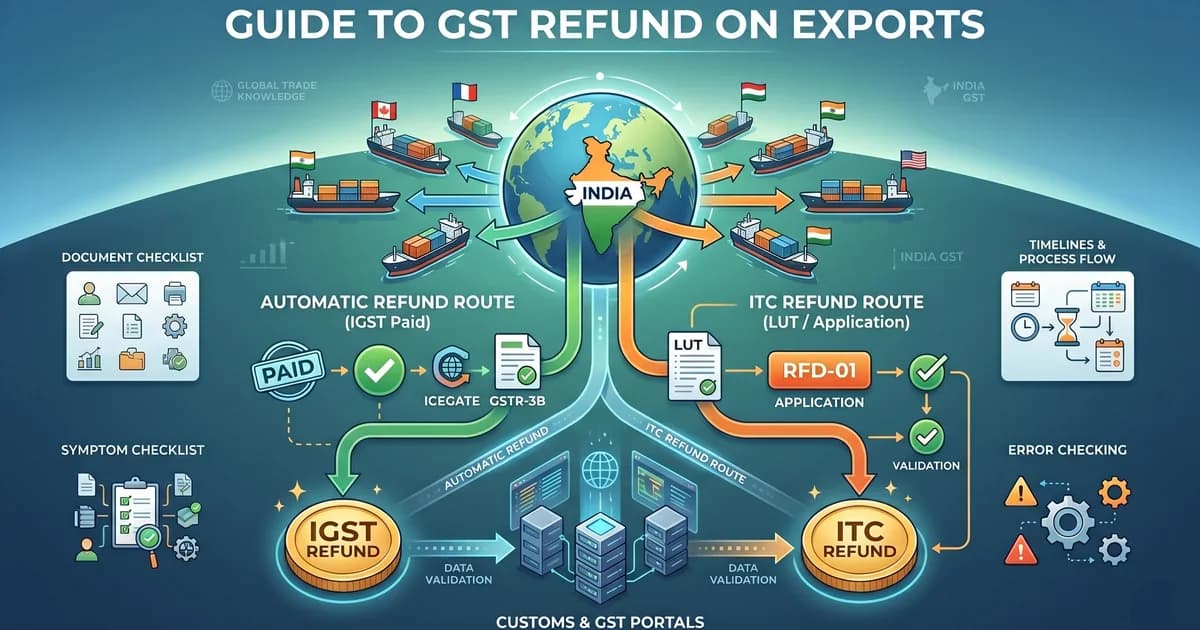

Two Routes for Exporters Under GST

Every exporter registered under GST has two options for handling the GST on their exports.

Route 1: Export Under LUT (No Upfront Tax)

You file a Letter of Undertaking (LUT) on the GST portal before exporting. With a valid LUT in place, you can raise export invoices with zero IGST. You are not collecting or paying any GST on the export sale.

You then claim a refund of the ITC accumulated on your inputs, the GST you paid to your domestic suppliers.

Route 2: Pay IGST and Claim Refund

You pay IGST on the export invoice at the applicable rate, using your ITC balance or cash. After the shipment is done and reflected in ICEGATE (the customs system), your shipping bill is automatically treated as a refund application. You receive 90% of the refund provisionally within 7 days of it being processed. The remaining 10% follows after document verification.

In most cases, the LUT route is more practical. Paying IGST upfront ties up your working capital and involves documentation scrutiny. LUT lets you export without any cash outflow on tax, and the ITC refund process is more straightforward.

LUT Eligibility: Who Can File?

Almost any GST-registered exporter can file an LUT. The main disqualification is a prosecution for tax evasion of ₹2.5 crore or more. If you are disqualified, you must use a bond with a bank guarantee instead.

- Valid GST registration (active GSTIN)

- No pending prosecution for tax evasion of ₹2.5 crore or more

- GST returns filed regularly with no outstanding dues

- LUT filed on the GST portal (Form GST RFD-11) before the first export of the financial year

- Renewed every financial year, valid April 1 to March 31

A textile manufacturer in Surat exports fabric worth ₹50 lakh to a buyer in the UAE. They have a valid LUT for FY 2026-27. Their export invoice shows ₹0 IGST. But they paid ₹3.5 lakh in GST on yarn, dyes, and packaging. They claim that ₹3.5 lakh as an ITC refund on the GST portal. No upfront tax payment, no blocked working capital.

Common Mistakes That Delay Refunds

These errors are the most common reasons refunds get stuck or rejected:

1. LUT not renewed on time. Your LUT expires on March 31 every year. Exporting without a valid LUT means your invoice is technically taxable. That is a costly compliance gap.

2. Mismatch between GSTR-1, GSTR-3B, and the shipping bill. Even small discrepancies in invoice numbers or values across these three documents can trigger an ICEGATE error (SB005) that blocks automatic refund processing.

3. Wrong invoice format. Export invoices must clearly state Supply Meant for Export Under LUT Without Payment of IGST or Supply Meant for Export Under Bond Without Payment of IGST. Missing this line puts the invoice in a compliance grey zone.

4. Claiming ITC on blocked credits. Under Section 17(5) of the CGST Act, certain inputs are blocked from ITC claims regardless of whether you export. These include motor vehicles for personal transport, food and beverages, and works contract services used for construction of an immovable property (such as a factory or office building). The block on works contracts is specific to construction of immovable property; sub-contractors who use works contract services as an input for onward supply of works contracts can still claim ITC.

Budget 2026: A Major Change for Service Exporters

Finance Act 2026, which received Presidential assent on 30 March 2026, deletes Section 13(8)(b) of the IGST Act with effect from that date. This provision previously classified Indian intermediary service providers (IT firms, BPO companies, digital agencies, and freelancers) as having their place of supply in India, forcing them to pay 18% GST on foreign-client revenues with no refund path. With the deletion, these services now fall under the default rule under Section 13(2): the place of supply is the recipient's location outside India. That converts them into zero-rated export services. If you run an IT or service firm with foreign clients, the change is already in effect. Consult your GST advisor to confirm your updated compliance position.

Frequently Asked Questions

Can I switch between LUT and IGST payment routes mid-year?

Yes. You can use both routes in different transactions within the same financial year, as long as you have a valid LUT for the transactions where you want to avoid upfront IGST.

Does missing a GST return affect my refund claim?

Yes. Refund applications are processed only if your GSTR-1 and GSTR-3B returns for the relevant period are filed. Pending returns block the refund workflow.

Do SEZ supplies need a separate LUT?

No. The same LUT covers both export of goods/services and supplies to SEZ units. However, the documentation required at the SEZ end differs. Consult the SEZ development commissioner's office for authorised operations compliance.

Is foreign remittance proof required for service export refunds?

Yes, for service exports. You need to show that payment was received in convertible foreign exchange (FIRC or Bank Realisation Certificate). For goods exports, the customs documentation via ICEGATE is the primary evidence.

Related Articles

- How to Get IEC (Import Export Code): Complete 2026 Guide. Your IEC is mandatory before your first export.

- How to File NIL GST Return. For months with no taxable transactions.

- LUT for Export Without GST: How to File RFD-11 (2026). The full RFD-11 process for filing your annual LUT.