Quick Summary

A GST refund on exports is what makes zero-rated supply actually zero-cost. You can recover either the IGST paid on the export invoice (Rule 96, automatic via ICEGATE) or the accumulated input tax credit built up under a Letter of Undertaking (Rule 89, via Form GST RFD-01). This guide covers both routes, the RFD-01 to RFD-06 flow, the 60-day timeline, ICEGATE error codes, and the mistakes that stall applications.

What You'll Learn

- How to claim a GST refund on exports through both the Rule 96 automatic route and the Rule 89 RFD-01 route

- What the RFD-01 to RFD-06 form workflow looks like, including the 7-day provisional refund and the 60-day final order

- How to fix the ICEGATE errors and compliance mismatches that block most exporter refunds

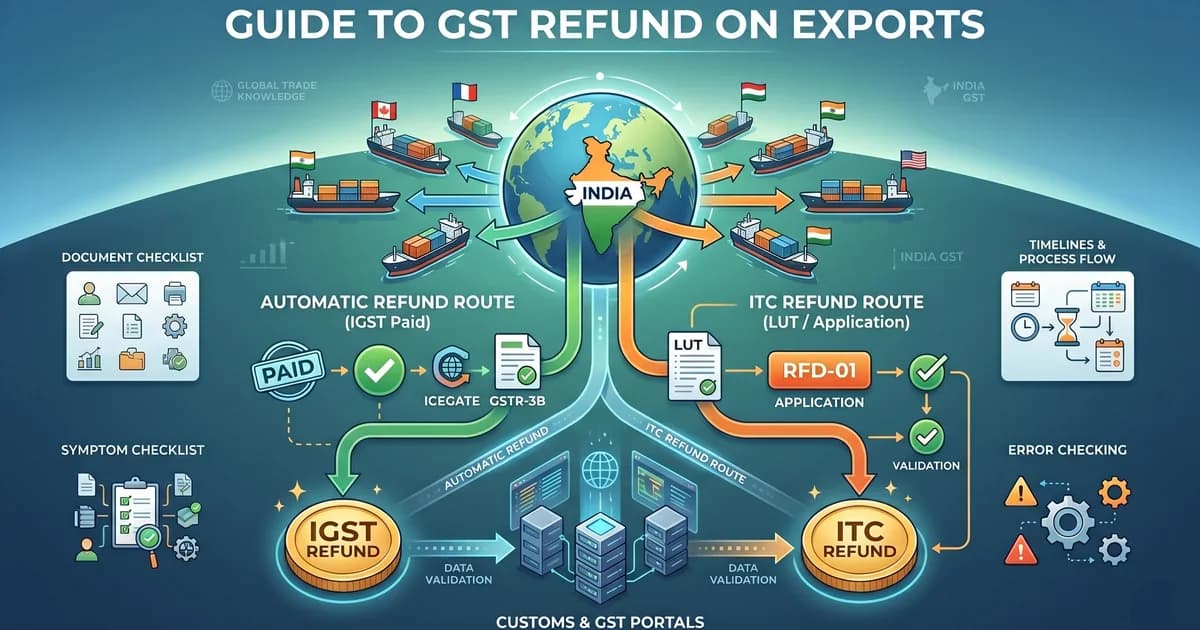

The Two Routes for GST Refund on Exports

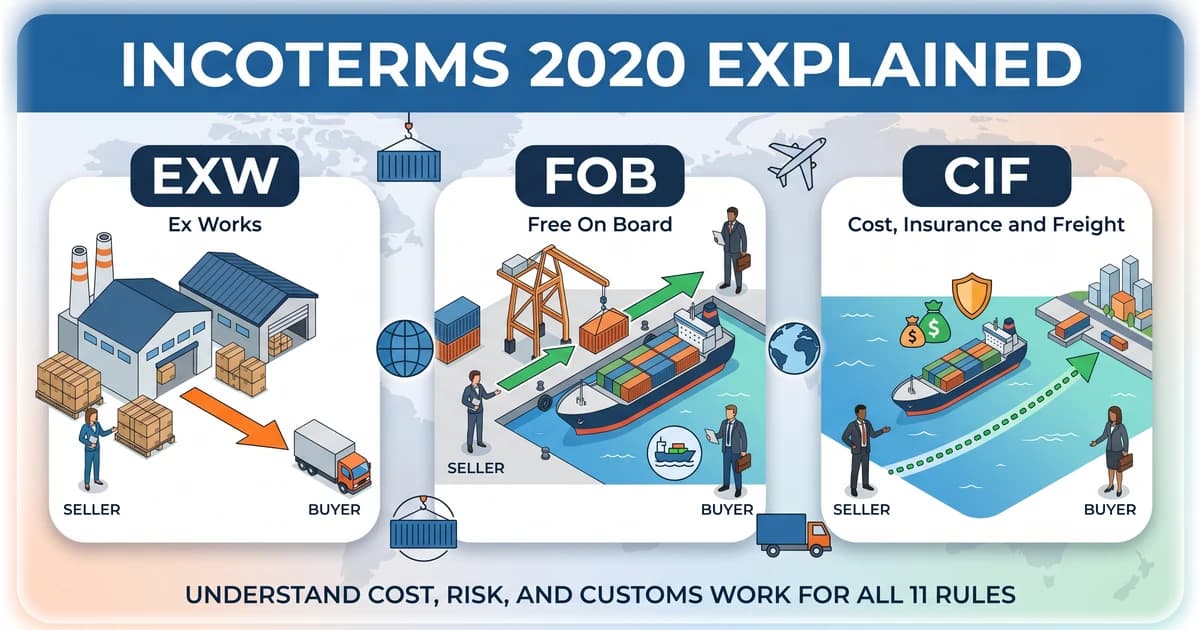

Exports from India are treated as zero-rated supplies under Section 16 of the IGST Act. That means you do not ultimately bear GST on an export sale, but you still need to actively reclaim the tax you paid somewhere in the chain. (For the legal concept of zero-rated supply, see our detailed guide on GST on Exports: Zero-Rated Supply Explained.)

There are exactly two routes, each governed by its own rule in the CGST Rules, 2017.

Rule 96: Automatic Refund of IGST Paid on Exports

You pay IGST on the export invoice and recover it after the goods ship. Under Rule 96, your shipping bill is itself deemed to be the refund application once the Export General Manifest (EGM) is filed and GSTR-3B is submitted for that tax period. No separate RFD-01 is needed.

Rule 89: Refund of Accumulated ITC Under LUT

You export without paying IGST, using a Letter of Undertaking (LUT), and later claim a refund of the input tax credit accumulated on your purchases. This route requires filing Form GST RFD-01 on the GST portal.

The LUT plus Rule 89 route is the working-capital-friendly choice for most regular exporters. You never pay IGST upfront, so no cash is blocked while you wait for a refund. Use the IGST-paid plus Rule 96 route only if your ITC balance is low, your LUT is not in force, or you are an occasional exporter whose export share is small.

Who Can Claim a GST Refund on Exports

You are eligible if:

- You have a valid GSTIN and your GSTR-1 and GSTR-3B filings are up to date.

- You hold a valid IEC from DGFT (required for export of goods). If you do not yet have one, start with our guide on how to get IEC registration.

- Your bank account is validated on the GST portal and linked to your GSTIN. Refunds are credited only to a validated account.

- For Rule 89, you hold a valid LUT for the financial year and your export invoice clearly marks the supply as one made under LUT without payment of IGST.

- You file within two years of the relevant date under Section 54 of the CGST Act. For goods, that is the date the ship or aircraft leaves India (or the date goods cross the frontier for land exports, or date of despatch for post). For services, it is the date of receipt of foreign exchange (or date of invoice where payment was received in advance).

Route 1: How to Claim a GST Refund Under Rule 96 (IGST Paid)

This is the more automated of the two routes. There is no RFD-01 to file. You just need your three data points (export invoice, shipping bill, GST returns) to match.

Step 1: File GSTR-1 with Table 6A Correctly

Report each export invoice in Table 6A of GSTR-1 with the shipping bill number, shipping bill date, port code, IGST rate, and IGST amount. Every character matters. A typo in the port code or shipping bill number is the single most common reason refunds get stuck.

Step 2: File GSTR-3B with Matching IGST

In Table 3.1(b) of GSTR-3B, report your zero-rated outward supplies with IGST paid. The IGST you report here must be equal to or greater than the IGST claimed in Table 6A of GSTR-1 for the same period. If 3B shows less IGST than 6A, the Customs system will not release the refund.

Step 3: Let the GST Portal Transmit Data to ICEGATE

Once GSTR-1 and GSTR-3B are filed, the GSTN system transmits invoice-level data to ICEGATE. ICEGATE matches it against the shipping bill and EGM. If the match is clean, the refund moves to disbursement.

Step 4: Receive the Refund to Your Bank

The refund lands in the bank account registered on ICEGATE. Typical processing is 7 to 15 days after the final data match. You can check status anytime under the GST validation report in your ICEGATE login.

A Mumbai leather goods exporter ships ₹20,00,000 worth of goods to Germany, paying 12% IGST (₹2,40,000) from ITC. The shipping bill is filed 3 April 2026, GSTR-1 on 11 May, GSTR-3B on 20 May. ICEGATE matches all three. The ₹2,40,000 refund lands by end of May, with no RFD-01 filed.

Route 2: How to File Form GST RFD-01 Under Rule 89

This is for exporters operating under LUT who want to recover the ITC sitting in their electronic credit ledger.

Step 1: Confirm All Prerequisites Are in Place

Before you open the refund form, verify:

- GSTR-1 and GSTR-3B for every period being claimed are filed.

- Your LUT for the current financial year is active on the portal.

- Your bank account is validated (check on the GST portal under My Profile → Bank Account).

Step 2: Complete the Refund Pre-Application Form

On the GST portal, go to Services → Refunds → Refund Pre-Application Form. This is a one-time disclosure of turnover, Aadhaar, and bank details. It must be filed before your first RFD-01.

Step 3: File Form GST RFD-01

Go to Services → Refunds → Application for Refund. Select the refund type Export of Goods/Services Without Payment of Tax or Supplies to SEZ Unit/Developer Without Payment of Tax, as applicable.

Pick the tax period (you can consolidate multiple periods in a single RFD-01). Upload Statement 3 for exports without payment of tax, Statement 4 for SEZ supplies, or Statement 5 for deemed exports. The portal auto-computes the refund using the Rule 89(4) formula:

Refund Amount = (Turnover of Zero-Rated Supply of Goods + Turnover of Zero-Rated Supply of Services) × Net ITC ÷ Adjusted Total Turnover

Under Rule 89(4)(C), Turnover of Zero-Rated Supply of Goods is capped at 1.5 times the value of like goods supplied domestically by the same or a similarly placed supplier, whichever is lower.

Step 4: Submit with DSC or EVC and Get Your ARN

Sign the application with a Digital Signature Certificate (companies and LLPs) or EVC (proprietors). The portal issues an Application Reference Number (ARN) immediately on successful submission. Save this ARN. It is how you track the file.

Step 5: Track the ARN

Track the ARN under Services → Refunds → Track Application Status. The file moves through a defined chain of forms, covered next.

The RFD-01 to RFD-06 Form Workflow

Knowing what each form means lets you know whether to wait, respond, or escalate.

| Form | Stage | What It Means | Typical Timeline |

|---|---|---|---|

| RFD-01 | Filed by exporter | Refund application submitted | Day 0 |

| RFD-02 | Acknowledgement | Application accepted as complete | Within 15 days |

| RFD-03 | Deficiency memo | Application is incomplete, resubmit | Within 15 days |

| RFD-04 | Provisional refund order | 90% of claim released provisionally | Within 7 days of RFD-02 |

| RFD-05 | Payment advice | Payment instructions sent to bank | After RFD-04 or RFD-06 |

| RFD-06 | Final refund order | Full refund sanctioned | Within 60 days of RFD-02 |

| RFD-08 | Show cause notice | Officer proposes to reject; respond in 15 days | Before RFD-06 |

Documents You Need

- Valid GSTIN, IEC, and active LUT for the financial year (for Rule 89 route)

- Export invoices with the legend Supply Meant for Export Under LUT Without Payment of IGST

- Shipping bills and Export General Manifest (EGM) for goods exports

- Bank Realisation Certificate (BRC) or FIRC for service exports and for ITC refund validation

- Statement 3 (exports without tax payment) or Statement 2 (exports with tax payment) in the prescribed format

- GSTR-1 and GSTR-3B returns filed for every period in the claim

- Bank account validated on the GST portal and linked to GSTIN

For Rule 96, ICEGATE pulls these from the shipping bill and EGM. For Rule 89, the statements and declarations are uploaded inside RFD-01.

Timelines and Interest on Delayed Refunds

| Event | Statutory Timeline |

|---|---|

| Acknowledgement in Form RFD-02 | Within 15 days of RFD-01 filing |

| Provisional refund (90%) in Form RFD-04 | Within 7 days of RFD-02 (zero-rated supplies) |

| Final refund order in Form RFD-06 | Within 60 days of RFD-02 |

| Interest on delayed refund | 6% per annum beyond 60 days, under Section 56 of CGST Act |

If the refund is not paid within 60 days of acknowledgement, interest at 6% per annum under Section 56 is automatically payable from day 61 until disbursement. No separate application is needed. The rate rises to 9% where the refund arises from an appellate or judicial order.

ICEGATE Error Codes That Block Exporter Refunds

Over 80% of stuck refunds on the Rule 96 route are caused by data validation failures between GSTN and ICEGATE. Knowing the error code tells you exactly where the fix is.

| Error Code | What It Means | How to Fix It |

|---|---|---|

| SB000 | Data successfully validated | No action needed, refund will flow |

| SB001 | Shipping bill number, date, or port code in Table 6A does not match the actual shipping bill | Amend Table 6A in the next GSTR-1 with correct shipping bill details |

| SB002 | EGM not filed by the shipping line | Approach the shipping line or CHA to file the EGM |

| SB003 | GSTIN on the shipping bill does not match the GSTIN filing GSTR-1 | Raise a correction request with the customs port officer |

| SB005 | Invoice number on the shipping bill does not match the invoice number in GSTR-1 | If the error is in GSTR-1, amend via Table 9A in the next return; if in the shipping bill, file a request with the customs officer using the approved Officer Interface |

| SB006 | EGM mismatch between the shipping bill and manifest | Request a supplementary EGM from the shipping line and revalidate at the gateway port |

Log into your ICEGATE account and open the GST Validation Status report before you chase anyone. It shows the exact error code against every shipping bill that failed validation. Fixing the actual code is faster than generic escalations to customs or the refund helpdesk.

Common Mistakes That Delay GST Refunds

1. LUT expired mid-year. An LUT is valid only from April 1 to March 31. Exports after April 1 without a renewed LUT are technically IGST-payable supplies, not zero-rated.

2. Invoice value mismatch across systems. The taxable value in GSTR-1 Table 6A, the ICEGATE invoice, and the shipping bill value must match to the rupee. Even a rounding mismatch triggers SB005.

3. GSTR-3B IGST lower than GSTR-1 Table 6A IGST. Customs will not sanction a refund larger than the IGST actually paid via 3B. Reconcile the two before filing.

4. Claiming blocked ITC in the Rule 89 formula. ITC on motor vehicles, food and beverages, and works contract services for construction of immovable property is blocked under Section 17(5). Including it triggers RFD-03.

5. Bank account not validated on the GST portal. Even a sanctioned RFD-06 cannot be disbursed to an unvalidated account. Validate before you file.

6. Missing the two-year window. Section 54 requires the application within two years of the relevant date. Exports from April 2024 must be claimed by April 2026; miss it and the entitlement is lost permanently.

Frequently Asked Questions

Can I claim a GST refund if I export without a valid LUT?

Yes, but only through the Rule 96 route. You must pay IGST on the export invoice and then recover it through the shipping bill as a deemed refund application. You cannot claim the Rule 89 accumulated ITC refund without an active LUT for that financial year.

How long does a GST refund on exports actually take?

Rule 96 clean applications disburse in 7 to 15 days after GSTR-1 and GSTR-3B. Rule 89 takes about 15 days for RFD-02, 7 days more for the 90% provisional RFD-04, and up to 60 days for final RFD-06. Delays beyond 60 days attract 6% interest under Section 56.

Do I need a Bank Realisation Certificate (BRC) for goods exports?

BRC is not required upfront for goods export refunds under Rule 96, because ICEGATE relies on the shipping bill and EGM. For service exports and for RFD-01 filings under Rule 89, BRC or FIRC is mandatory proof that convertible foreign exchange was received.

What if the officer issues a deficiency memo or rejection notice?

A deficiency memo (RFD-03) means the application is incomplete. Fix the gap and file a fresh RFD-01 for the same period. A show cause notice (RFD-08) proposes rejection; you have 15 days to respond via RFD-09. If rejection follows in RFD-06, you can appeal under Section 107 of the CGST Act.

Can I combine multiple tax periods in one RFD-01?

Yes. You can club tax periods in a single RFD-01 for zero-rated supplies, including across different financial years. The earlier same-FY restriction was removed by CBIC Circular 135/05/2020 dated 31 March 2020. Clubbing reduces administrative load and helps meet the minimum claim threshold.

Related Articles

- GST on Exports: Zero-Rated Supply Explained

- How to Get IEC (Import Export Code): Complete 2026 Guide

- How to File NIL GST Return

- LUT for Export Without GST: How to File RFD-11 (2026)