Quick Summary

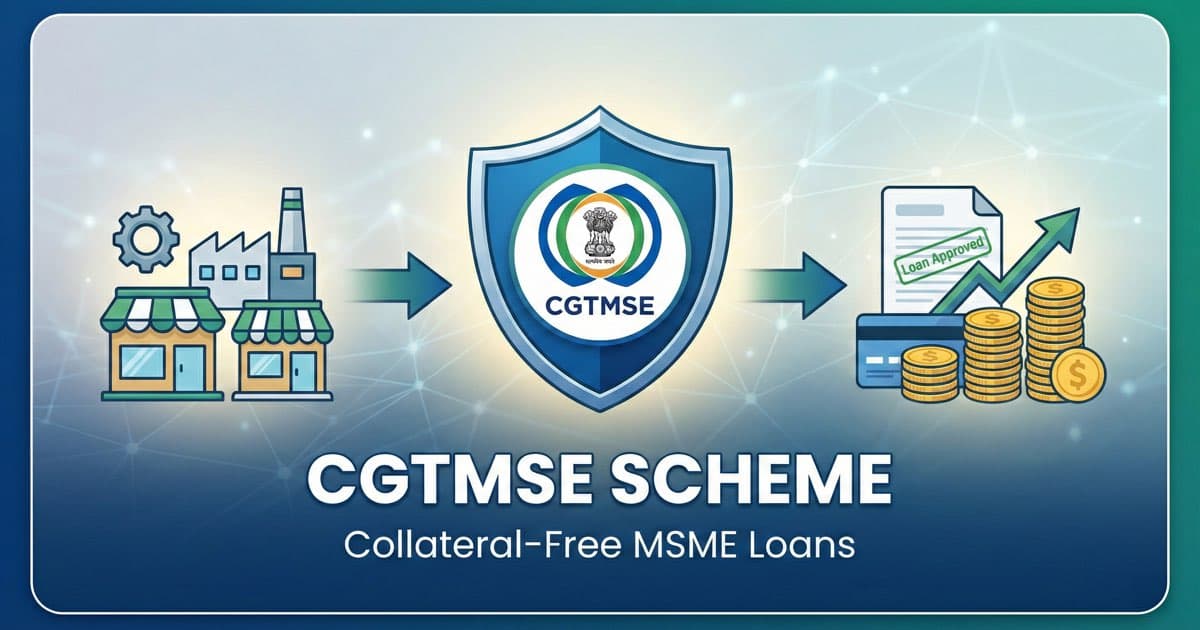

The CGTMSE loan scheme removes the biggest barrier for MSMEs seeking bank credit: collateral. Instead of pledging property, the government-backed trust guarantees 75-90% of your loan, covering amounts up to ₹10 Crore. This guide covers who qualifies, guarantee coverage and fees (revised April 2025), the step-by-step application process, and practical tips to get your loan approved.

What You'll Learn

- How to access collateral-free MSME loans up to ₹10 Crore through CGTMSE-registered banks and NBFCs

- What eligibility criteria, documents, and prerequisites you need before approaching a lender

- How to strengthen your loan application and what actually happens if you default

What is the CGTMSE Scheme?

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) is a government initiative launched in August 2000 by the Ministry of MSME and the Small Industries Development Bank of India (SIDBI). Its purpose is straightforward: help MSMEs get bank loans without pledging personal property.

Here's how it works. When you apply for a business loan, banks typically ask for collateral (land, property, fixed deposits). Most small business owners don't have assets to pledge. CGTMSE steps in as a government-backed guarantor. If your loan goes bad, the trust compensates the bank for a significant portion of the loss.

This safety net encourages banks to lend based on the viability of your business rather than the value of your assets.

You don't apply to CGTMSE directly. You approach a bank or NBFC registered as a Member Lending Institution (MLI), and the lender applies for guarantee coverage on your behalf after sanctioning your loan.

Who Can Apply?

Eligible Businesses

The CGTMSE scheme covers new and existing Micro and Small Enterprises engaged in:

- Manufacturing (production, assembly, processing)

- Services (IT, consulting, healthcare, hospitality)

- Retail Trade (shops, showrooms)

- Wholesale Trade (distribution, bulk trading)

Trading activities were aligned with manufacturing and services under the revised scheme in 2025, meaning traders now get the same coverage rates and fee structure.

Key Requirements

| Requirement | Details |

|---|---|

| Udyam Registration | Mandatory for all applicants |

| IT PAN | Required for loans above ₹5 lakh (recommended for all) |

| Loan Default History | Must not be a defaulter with any financial institution |

| Entity Type | Proprietorship, partnership, private limited, LLP |

| Enterprise Size | Must classify as Micro or Small under MSMED Act |

Who Does NOT Qualify?

- Medium Enterprises (only Micro and Small are covered)

- Agricultural activities

- Self-Help Groups (SHGs) and Joint Liability Groups

- Educational and training institutions (under main CGS-I scheme)

Medium enterprises are NOT covered under CGTMSE. Your enterprise must qualify as Micro (investment up to ₹1 Cr, turnover up to ₹5 Cr) or Small (investment up to ₹10 Cr, turnover up to ₹50 Cr) as defined in your Udyam Registration.

How Much Can You Borrow?

Guarantee Ceiling

As of April 1, 2025, the maximum guarantee coverage has been doubled from ₹5 Crore to ₹10 Crore. This means you can get collateral-free loans up to ₹10 Crore under a single CGTMSE guarantee.

For loan requirements exceeding ₹10 Crore, a hybrid model is available. You provide collateral for the portion above ₹10 Crore, and the unsecured portion (up to ₹10 Crore) gets CGTMSE coverage.

Guarantee Coverage by Category

The trust doesn't cover 100% of the loan. Coverage varies by borrower category:

| Borrower Category | Coverage |

|---|---|

| Micro Enterprises (up to ₹5 Lakh) | 85% |

| Women / Agniveers | 90% |

| SC / ST / PwD Entrepreneurs | 85% |

| ZED Certified Units | 85% |

| NE Region, J&K, and Ladakh (up to ₹50 Lakh) | 80% |

| All other categories (above ₹50 Lakh) | 75% |

Units in credit-deficient districts identified by the government receive an additional 5% coverage above their applicable rate.

Annual Guarantee Fee (AGF)

You pay a yearly fee to maintain the guarantee. The revised slab structure (effective April 2025) significantly reduced costs:

| Loan Amount | AGF Rate (per year) |

|---|---|

| Up to ₹10 Lakh | 0.37% |

| ₹10 Lakh - ₹50 Lakh | 0.55% |

| ₹50 Lakh - ₹1 Crore | 0.60% |

| ₹1 Crore - ₹2 Crore | 0.85% |

| ₹2 Crore - ₹5 Crore | 1.00% |

| ₹5 Crore - ₹8 Crore | 1.10% |

| ₹8 Crore - ₹10 Crore | 1.20% |

The fee is calculated on the outstanding loan balance and decreases as you repay your principal. All rates are exclusive of GST.

Interest Rates

CGTMSE does not set interest rates. Your lender decides the rate based on their own credit assessment. Typical ranges in 2026:

- Public Sector Banks: 8.50% - 12.00% p.a.

- Private Banks: 10.00% - 16.00% p.a.

- NBFCs: 14.00% - 22.00% p.a.

A textile manufacturer in Surat borrows ₹25 lakh from SBI under CGTMSE. As a general category borrower, 75% of the loan (₹18.75 lakh) is guaranteed by CGTMSE. The annual guarantee fee for the first year is 0.55% of ₹25 lakh = ₹13,750 (plus GST). If the interest rate is 10% p.a., the total first-year cost is roughly ₹2.5 lakh in interest + ₹13,750 in AGF.

How to Apply for a CGTMSE Loan

Step 1: Complete Udyam Registration

If you don't have Udyam Registration yet, complete it first at udyamregistration.gov.in. It's free and takes about 10 minutes. Your Udyam number is mandatory for any CGTMSE application.

Step 2: Prepare Your Documents

- Udyam Registration Certificate

- PAN card of the business and promoter(s)

- KYC documents (Aadhaar, address proof)

- Detailed Project Report (DPR) with financial projections

- ITR and audited financials for the last 2-3 years

- Bank statements for the last 12 months

- GST returns (if registered)

- Business registration certificate (Partnership deed, MOA/AOA, etc.)

For new businesses without financial history, a strong DPR is especially important. It should cover your business model, market potential, revenue projections, and how you plan to use the funds.

Step 3: Find a Member Lending Institution (MLI)

Not every bank or NBFC participates in CGTMSE. You can find registered Member Lending Institutions on the CGTMSE website under the Credit Guarantee Scheme sections. Major MLIs include SBI, Bank of Baroda, Canara Bank, HDFC Bank, ICICI Bank, and several NBFCs.

Step 4: Submit Your Loan Application

Approach your chosen MLI and apply for a business loan. Mention that you want CGTMSE coverage. The bank processes your application through their standard credit appraisal, evaluating your business viability, repayment capacity, and credit history.

Step 5: Bank Sanctions and Applies for Guarantee

Once the bank approves your loan, they apply to CGTMSE for guarantee coverage. CGTMSE reviews the application and issues the guarantee upon receiving the annual fee.

Step 6: Loan Disbursed Without Collateral

After guarantee approval, your loan is disbursed. No property, no third-party guarantors. You start repaying as per the agreed schedule.

Typical processing time from application to disbursement is 1-3 weeks, depending on the lender and the completeness of your documentation.

Tips to Strengthen Your Application

Banks still bear 10-25% of the risk even with CGTMSE coverage. A strong application matters.

- Maintain a CIBIL score of 700+: Banks check your personal credit score. A business CMR rank between 1 and 4 is also preferred.

- Write a solid DPR: Generic project reports get rejected. Include realistic revenue projections backed by market data, a clear use-of-funds breakdown, and your repayment plan.

- Keep clean financials: Consistent GST filings and healthy bank statements (12 months minimum) signal reliability. Irregular cash flows or unexplained large transactions raise red flags.

- Use the guarantee calculator: CGTMSE offers an online Guarantee Calculator to estimate your guarantee coverage and fees before you apply.

Start with your existing bank where you already have a current account or savings account. Banks are significantly more likely to approve CGTMSE loans for customers with an established banking relationship and visible transaction history.

What Happens If You Default?

Understanding default consequences helps you plan responsibly.

- The bank marks your loan as a Non-Performing Asset (NPA)

- The bank initiates legal recovery proceedings against you

- The bank files a claim with CGTMSE for the guaranteed portion

- CGTMSE pays the bank 75% of the eligible claim within 30 days

- The remaining balance is settled after recovery proceedings conclude

For claims up to ₹5 lakh, the legal action requirement is waived by CGTMSE.

The guarantee covers the lender's risk, not yours. If you default, the bank will still pursue legal recovery against you for the uncovered portion of the loan. A default also severely damages your credit score and disqualifies you from future CGTMSE loans.

Frequently Asked Questions

QCan a new startup get a CGTMSE loan?

Yes. Both new and existing Micro and Small Enterprises can apply. For new businesses, a detailed and viable project report (DPR) is essential since you won't have financial history to show.

QDoes CGTMSE cover retail and wholesale traders?

Yes. As of the April 2025 revisions, trading activities (both retail and wholesale) are fully covered under CGTMSE with the same guarantee rates and fees as manufacturing and service units.

QCan I convert an existing collateralized loan to CGTMSE?

Generally no. CGTMSE covers new and fresh credit facilities. However, some banks may allow releasing collateral for well-performing accounts by shifting them under CGTMSE coverage. Check with your specific lender.

QWhat is the typical loan tenure?

For term loans, tenure is usually 5-7 years. For working capital (Cash Credit/Overdraft), limits are renewed annually for blocks of up to 5 years.

QCan I apply directly on the CGTMSE website?

No. MSMEs cannot apply to CGTMSE directly. You must approach a CGTMSE-registered bank or NBFC (Member Lending Institution) and apply for the loan through them. The bank then applies to CGTMSE for guarantee coverage.

QIs Udyam Registration mandatory for CGTMSE?

Yes. Udyam Registration is a prerequisite. You cannot access any CGTMSE-backed loan without a valid Udyam Registration number.

Related Articles

- Startup India Registration: DPIIT Benefits Guide - If your MSME is also an innovative startup, combine CGTMSE credit with DPIIT recognition benefits

- What is Udyam Registration? Complete Guide for MSMEs - Udyam Registration is mandatory for CGTMSE. Complete it first if you haven't already

Scheme details and fee structures are subject to revision. Always verify current information on the official CGTMSE website and with your chosen lending institution before applying.