Quick Summary

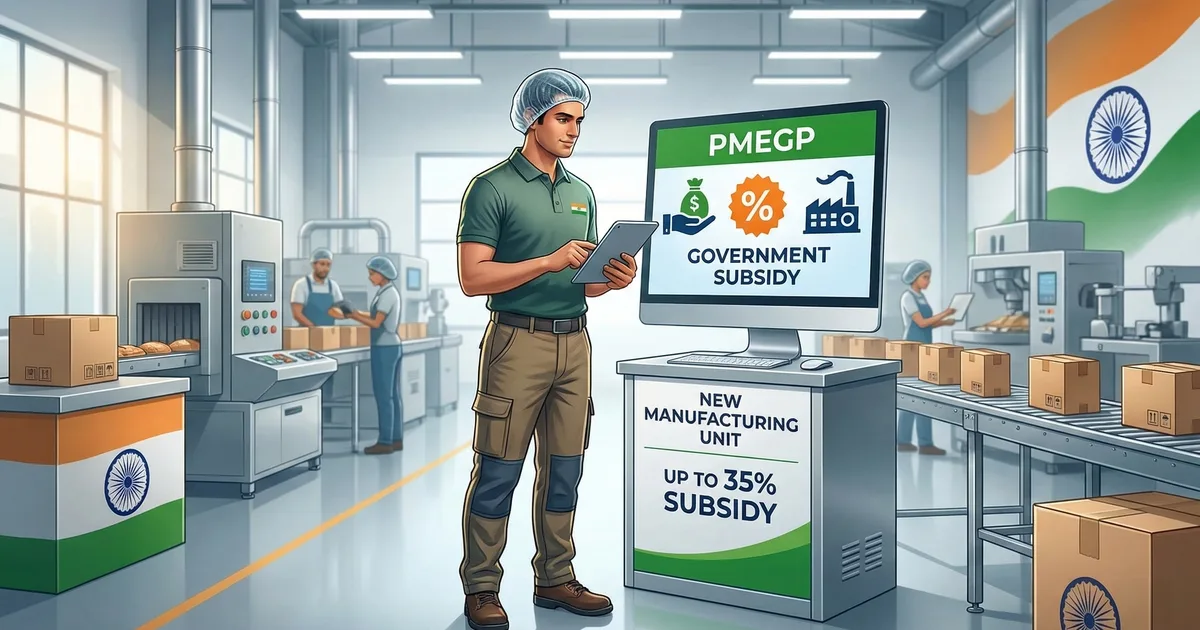

PMEGP (Prime Minister's Employment Generation Programme) provides government-backed bank loans with a direct subsidy of 15-35% for new manufacturing and service units. The subsidy is not given as cash — it is locked in your loan account for 3 years, then adjusted against your outstanding balance to reduce repayment. This guide covers who meets PMEGP scheme eligibility criteria, how the margin money subsidy actually works, project cost limits (up to ₹50 lakh for manufacturing), and the step-by-step application process on the KVIC portal.

What You'll Learn

- How to determine if you meet PMEGP scheme eligibility criteria and what common disqualifiers to watch for

- What subsidy rates apply to your category and how the margin money is adjusted in your loan account

- How to complete the PMEGP application process from the KVIC portal through to loan disbursement

What is the PMEGP Scheme?

The Prime Minister's Employment Generation Programme (PMEGP) is a credit-linked subsidy scheme run by the Ministry of MSME through the Khadi and Village Industries Commission (KVIC) as the single national nodal agency. It was launched in 2008 by merging two earlier programmes: PMRY (Prime Minister's Rozgar Yojana) and REGP (Rural Employment Generation Programme).

The scheme solves a real problem: a first-time entrepreneur has a viable business idea but cannot arrange the full capital to start. PMEGP bridges this gap by having a bank fund most of the project cost while the government contributes a non-repayable portion called margin money.

The scheme was sanctioned under the 15th Finance Commission cycle (2021-22 to 2025-26). Project cost limits were revised upward in May 2022, raising the manufacturing ceiling from ₹25 lakh to ₹50 lakh and the service sector ceiling from ₹10 lakh to ₹20 lakh.

PMEGP is exclusively for setting up new enterprises. If your business already exists, you cannot apply — even for expansion. The scheme funds first-time ventures only.

PMEGP Scheme Eligibility

Who Can Apply?

PMEGP is open to both individuals and institutions:

| Applicant Type | Details |

|---|---|

| Individual Entrepreneurs | Indian citizen, 18 years or above |

| Self-Help Groups (SHGs) | Only SHGs that have not received benefits under other government schemes |

| Registered Societies | Institutions registered under the Societies Registration Act, 1860 |

| Production Cooperatives | Cooperative societies engaged in production activities |

| Charitable Trusts | Registered trusts involved in productive activity |

There is no income ceiling. You do not need to prove you are below a certain income level to apply.

Education Requirement

For most applicants, no specific qualification is required. However, if your project cost exceeds certain thresholds, you need at least an 8th standard pass certificate:

- Manufacturing projects costing above ₹10 lakh: 8th standard minimum

- Service/business projects costing above ₹5 lakh: 8th standard minimum

Who Cannot Apply?

You are NOT eligible for PMEGP if your business already exists (only new projects qualify), you have previously received a margin money subsidy under PMEGP or any other government scheme, you are a loan defaulter with any bank or financial institution, or your planned activity falls under the PMEGP negative list (tobacco, meat processing, plantation farming, poultry, etc.). Check the full list before finalising your business activity.

How Much Subsidy Can You Get?

PMEGP offers a margin money subsidy ranging from 15% to 35% of the project cost, depending on your category and location. You also need to contribute a small portion from your own pocket. The bank funds the rest as a loan.

Subsidy and Contribution Breakdown

| Category | Area | Own Contribution | Govt. Subsidy | Bank Loan |

|---|---|---|---|---|

| General | Urban | 10% | 15% | 75% |

| General | Rural | 10% | 25% | 65% |

| Special* | Urban | 5% | 25% | 70% |

| Special* | Rural | 5% | 35% | 60% |

*Special category includes: SC/ST, OBC, Minorities, Women, Transgender, Ex-Servicemen, Physically Handicapped, and applicants from the North East Region (NER), Aspirational Districts, Hill areas, and Border areas.

A woman entrepreneur in rural Rajasthan sets up a food processing unit with a total project cost of ₹30 lakh (manufacturing sector). As a Special category applicant in a rural area, she qualifies for a 35% subsidy.

- Own contribution: 5% = ₹1.5 lakh

- Government subsidy (margin money): 35% = ₹10.5 lakh

- Bank loan: 60% = ₹18 lakh

She needs only ₹1.5 lakh from her own pocket to start a ₹30 lakh unit. The ₹10.5 lakh subsidy stays locked in her loan account for 3 years. After that, if the unit is operational and repayments are on track, the subsidy is adjusted against the outstanding loan balance. Her effective repayment drops from ₹18 lakh to ₹7.5 lakh.

How the Subsidy Actually Reaches You

The subsidy does not arrive as cash. Here is what happens after your loan is sanctioned:

- The bank disburses funds so you can set up your unit

- KVIC routes the margin money to a separate subsidy account linked to your loan

- The subsidy remains locked in this account for a 3-year lock-in period

- After 3 years of regular repayment and operational verification, the subsidy is adjusted against your outstanding loan balance

- Your repayment burden reduces significantly from the 4th year onward

The interest rate on the loan follows the bank's standard MSME lending norms.

Project Cost Limits

| Sector | Maximum Project Cost |

|---|---|

| Manufacturing | ₹50 lakh |

| Service / Business | ₹20 lakh |

The project cost includes machinery, equipment, furniture, one cycle of working capital, and other eligible capital expenditure. Two important exclusions apply:

- Land cost is not included in the project cost calculation under any circumstances.

- Projects without capital expenditure are not eligible — the scheme requires a physical productive asset to be created.

Costs above the sectoral ceilings are not covered by the scheme.

Activities NOT Covered Under PMEGP

Not every business qualifies. The PMEGP negative list explicitly excludes:

- Food and beverages: Businesses involving slaughtered meat processing or canning, tobacco products (beedi, cigar, cigarette), liquor retail outlets, toddy tapping, and dhabas or hotels that serve liquor

- Agriculture and allied: Crop cultivation, plantation farming (tea, coffee, rubber), sericulture (cocoon rearing), horticulture, floriculture, animal husbandry including poultry, piggery, and pisciculture

- Manufacturing: Polythene carry bags under 20 microns, recycled plastic containers used for food storage or packaging

- Transport: Rural transport in most states (limited exceptions apply: Auto Rickshaws in Andaman & Nicobar Islands, houseboats and shikaras in Jammu & Kashmir, and cycle rickshaws)

Always verify your chosen activity against the full official negative list on the KVIC PMEGP portal before submitting your application.

How to Apply for PMEGP

The entire application process is online through the KVIC e-Portal at kviconline.gov.in/pmegpeportal.

Step 1: Register on the KVIC Portal

Validate your Aadhaar details on the portal. You will receive a User ID and Password via SMS. Use these to log in and start your application.

Step 2: Fill the Application Form

Complete the application online. You will need to select your business sector, enter the estimated project cost, choose your sponsoring agency (KVIC, KVIB, or DIC), and fill in the online Score Card that assesses your business profile.

Step 3: Upload Documents and Submit

- Aadhaar Card (mandatory for portal validation)

- PAN Card

- Passport-size photographs

- Caste or category certificate (if applying as Special category)

- 8th pass certificate (if project cost exceeds ₹10L for manufacturing or ₹5L for service)

- Detailed Project Report (DPR) with financial projections and employment plan

- Quotations for machinery and equipment to be purchased

- Proof of business premises (rent agreement or ownership proof)

- Bank account details

- Affidavit or declaration as per scheme format

After uploading all documents, take a printout of the online application and submit it physically to your nearest KVIC, KVIB, or DIC office along with the DPR and supporting papers.

Step 4: Scrutiny by Sponsoring Agency

Your KVIC/KVIB/DIC office reviews the application and may call you for an interview. They assess the business viability and employment potential. If approved, they forward the application to the financing bank.

Step 5: Bank Appraisal and Loan Sanction

The bank conducts a standard credit appraisal, reviewing your project report, repayment capacity, and credit history. Projects up to ₹5 lakh are exempt from collateral. Projects between ₹5 lakh and ₹25 lakh receive a CGTMSE-backed collateral guarantee automatically. Once satisfied, the bank sanctions the loan.

Step 6: EDP Training — Mandatory Before First Disbursement

This is where many applicants are caught off-guard. Before your first loan installment is released, you must complete an Entrepreneurship Development Programme (EDP). You have two options:

-

Online (Recommended): Conducted via the Udyami Portal.

- Duration: 15 days

- Cost: Free of cost for PMEGP beneficiaries whose loan has been sanctioned (previously chargeable).

- How to Access: Log in using your registered mobile number from the PMEGP portal.

-

Offline (Physical): Conducted at RSETI, RUDSETI, or KVIC training centers.

- Duration: 6 working days (for projects up to ₹5 lakh) or 10 working days (for projects above ₹5 lakh).

- Cost: Chargeable (approx. ₹3,000–₹6,000 depending on the institute and course duration), unless covered by specific state waivers.

The training covers business planning, financial literacy, marketing, and compliance basics.

Step 7: Loan Disbursement and Subsidy Lock-in

After EDP completion, the bank disburses the loan and you can begin setting up your unit. KVIC routes the margin money into your locked subsidy account. You repay the bank EMIs as scheduled. After 3 years of satisfactory performance, the subsidy is adjusted to reduce your outstanding balance.

The Detailed Project Report (DPR) is the single most important document for getting PMEGP approval. Banks and scrutiny committees reject generic templates. Your DPR must include realistic revenue projections backed by market data, a clear use-of-funds breakdown, an employment generation plan, and a credible repayment schedule. KVIC provides model project templates for common manufacturing activities on the e-Portal. Use them as a starting reference only, not as copy-paste documents.

Can You Apply for a Second Loan?

If your PMEGP-funded unit performs well, you can apply for second financial assistance to expand or upgrade:

| Sector | Max. Project Cost | Subsidy Rate | Max. Subsidy |

|---|---|---|---|

| Manufacturing | ₹1 crore | 15% (20% for NER/Hill states) | ₹15 lakh (₹20 lakh for NER) |

| Service / Trading | ₹25 lakh | 15% (20% for NER/Hill states) | ₹3.75 lakh (₹5 lakh for NER) |

To qualify for a second loan, all three conditions must be met:

- Your margin money from the first loan must have been adjusted (i.e., the 3-year lock-in completed)

- Your first loan must be fully repaid on schedule

- Your unit must have been operational and profitable for at least 3 consecutive years (as required under official second-loan guidelines from the Ministry of MSME)

Official Resources

- PMEGP e-Portal — Start your application here on the KVIC website

- Udyami Portal (EDP Training) — Official platform for mandatory online EDP training

- Ministry of MSME — Eligibility Criteria — Official eligibility page with scheme details

- KVIC Negative List — Full list of activities not covered under PMEGP

- KVIC How to Apply Guide — Step-by-step application and EDP training details

Related Articles

- MSME Loans Under CGTMSE Scheme: How to Apply — PMEGP projects between ₹5 lakh and ₹25 lakh automatically receive CGTMSE collateral coverage. Read this to understand how the guarantee scheme works beyond PMEGP

- Government Tenders for MSME: How to Win Contracts — Once your unit is operational, government procurement gives MSME suppliers a 25% reservation and reliable domestic demand

- Startup India Registration: DPIIT Benefits Guide — If your manufacturing unit involves innovation, DPIIT recognition adds tax exemptions and compliance benefits alongside PMEGP

- What is Udyam Registration? Complete Guide for MSMEs — Register on Udyam after PMEGP approval to access the full range of MSME benefits, priority sector lending, and government scheme eligibility

Scheme details, subsidy rates, and project cost limits are subject to revision at the end of each Finance Commission cycle. Always verify current guidelines on the official KVIC portal or the Ministry of MSME website before applying.